If you’re reading this, there is a good chance that you’ve been told by a doctor that you have high blood pressure. For many of you, you’ve been putting off applying for life insurance and now you’re concerned that you’re going to be denied or asked to pay more for coverage. If this is you, you’re in the right place! Life insurance companies insure millions of people every year with high blood pressure. Requirements will vary from insurer to insurer but if you stay with me and follow my advice, I’m going to walk you through on how to get the best policy and premium to fit your needs.

What is High Blood Pressure?

Before we get to the specifics on how life insurance companies view and underwrite for high blood pressure let’s take a second and clear up any confusion you may have about your diagnosis. High blood pressure or hypertension is a condition where your blood is exerting too much pressure against the walls of your arteries and veins. The reading that you commonly get from your doctor is made up of two readings: systolic pressure (the top number) and diastolic pressure (the bottom number). Systolic pressure is the pressure as your heart contracts. Diastolic pressure is the pressure as your heart relaxes. Readings from 120/80 to 129/80 are considered elevated. Readings above 130/80 are generally considered high.

So what’s so wrong with having high blood pressure? Your doctor is concerned (and you should be too!) with the issues that come with high blood pressure such as kidney problems, heart disease, damage to your eyes, and even stroke.

High blood pressure can affect the premium you will pay and ultimately whether or not you get coverage at all.

3 Misconceptions Concerning High Blood Pressure

There are a number of misconceptions concerning your high blood pressure that I come across on a regular basis.

Misconception #1: If I’ve been diagnosed with high blood pressure I can not qualify for the best rates.

This statement is absolutely wrong! We help clients on a weekly basis qualify for preferred-best rates with high blood pressure. Hypertension isn’t a life insurance death sentence! If you’ve heard this, it’s likely that another person or perhaps an inexperienced insurance agent has mentioned this in conversation. If it was an agent, this is a potential red flag and a warning that his or her company isn’t very good with blood pressure.

Example:

At the writing of this, I just finished helping “J.T.,” who is a personal friend of mine and a local banker here in Birmingham qualify for preferred-best rates on a $1.5 Million dollar life insurance policy. When Jeremy and I began this process a little more than a month ago, he had a few readings in the 135/80 range and was close to being medicated for blood pressure. To get J.T. the best rates, I narrowed his options down to three life insurance companies who were very forgiving on their B.P. requirements. I then had a conversation with my underwriter at each of these life insurers and applied with the company that gave us the best chances for preferred-best rates.

Misconception #2: Taking blood pressure medications will disqualify me for the best rates.

Another falsehood. The truth is actually just the opposite. If you’ve been diagnosed with high blood pressure, life insurance companies would prefer that you take a medicine for blood pressure. The idea here is that underwriters are wanting to see that you’re meeting with your physician and following the plan. Meeting with your physician following orders equals control and control equals good results and better premiums. The opposite is true as well. If you have high blood pressure and you don’t see your doctor or take your prescriptions, you’re going to pay more. It’s that simple.

If you’ve been diagnosed with high blood pressure, life insurance companies would prefer that you take a medicine for blood pressure.

Misconception # 3: All or most life insurance companies underwrite for blood pressure the same.

Premiums are generally the same from insurer to insurer is another variant of this misconception. Both of these misconceptions are far from the truth. As an independent broker for life insurance, I currently have access to 30-40 life insurance companies and just about every one of them has different requirements for blood pressure. Consequently, the problem for applicants is that underwriting for insurance is extremely “either, or.” You either fit an insurance company’s requirements or you don’t. Even one point over a particular blood pressure requirement can cause you to drop a rate class. The difference between rate classes can mean upwards of 25% more in premium for the same amount of coverage!

Example: Underwriting Requirements For Various Life Insurance Companies

Blood Pressure Underwriting Requirements For Three Life Insurers

The examples to the left are underwriting requirements for blood pressure. I’ve hidden the names of the insurers because insurance companies have entire departments consisting of attorneys. I do not. You’ll notice a number of variables in the chart: age, BP measurements, type of insurance being applied for, average readings, length of control and treatment.

How Does Underwriting Work With an Actual Client?

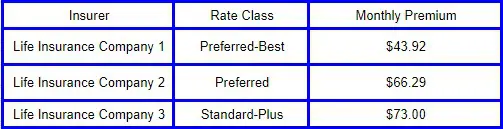

Every time I work with a client with high blood pressure, I compare their readings with insurance company requirements. But what do they look like for an actual client? Let’s look at a 40-year-old female, applying for $1M in coverage. She has been diagnosed eight months ago with high blood pressure with an average reading of 140/85 She saw her doctor and began treatment with a medication and after six months now has an average reading of 134/84. What would the premium look like for our applicant after applying for coverage?

Life insurance company 1 wins this one as she can still conceivably qualify for preferred-best rates. Insurer 2 would underwrite her at preferred rates because her average reading is too high for preferred-best rates. Insurance company 3 would be the worst of the three companies represented because they have a two-year requirement for average readings. Our applicant here has only been controlled for 6 months, therefore, she wouldn’t be a good fit for insurer 3.

Example: Various Premiums for High Blood Pressure.

The takeaway here is that there are a number of factors that go into your premium! In this hypothetical example, selecting the right company saved her as much as 40% between company 1 and 3!

3 Steps to Take if You’re Applying With High BP

1. Work With An Independent Agent:

First of all, you need to consider working with an independent agent or broker for life insurance. This goes without saying as getting the best rates requires that you have more options! A good independent agent with a strong track record of working with high blood pressure clients will make a world of difference. If you’re working with a captive agent who is an employee of an insurance company, it’s going to be in your best interest to get a second opinion.

2. See Your Doctor and Follow Their Orders:

Life insurance and high-blood pressure aside, this is just a good rule of thumb for everyone. Even for the men reading this who are generally reluctant to see a doctor. Swallow your pride and see your doctor. But whether we’re talking blood pressure, cholesterol, or any other issue you’re being treated for— life insurance companies like to see control. Remember, control to your underwriting means you’re seeing your doctor and taking your meds.

3. Wait at Least Six Months before Applying:

Third, blood pressure control to an underwriter means control for a minimum of six months. Hence you’ll need to have good readings for a period of at least six months. So from the first appointment, your doctor diagnosed you with high blood pressure and prescribed a medication to your second appointment six months later. If your readings have been lower and steady for six months it’s safe to start asking your independent agent questions. For many people though, it may take more than six months to get your BP under control. People respond differently to various medications. So it may well take up to a year and beyond in some cases to get your readings under control.

Have You Been Diagnosed With High Blood Pressure?

We’ve helped countless people over the years with high blood pressure to get the best policy and premium. Whether you’re curious if you have the best rates or if you’re just beginning to ask questions about what life insurance would look like now that you have hypertension, don’t hesitate to contact us. There is always no obligation, even if you’re just looking for a second opinion.

Sam Price is an independent insurance agent and broker in Birmingham, AL. He works hard every day to give his clients access to over 30 of the most trusted, A+ rated life insurance companies in the country— more access means better premiums and more coverage.